Key Takeaways

- Despite rapid renewable expansion, China continues to build and commission new coal-fired power plants and increases raw coal production. This persistence reflects the coal sector’s deep economic and political role in China’s development model.

- China still lacks a coherent, targeted coal phase-out strategy. Decarbonization remains fragmented, with coal-dependent, resource-depleted cities offering early insights into the challenges ahead. Their common responses include diversifying into heavy industry and expanding tourism.

- Coal-dependent cities face major structural constraints: slowing growth, population decline, and limited investment capacity. In many underdeveloped regions, these pressures make economic transition difficult and reinforce continued reliance on coal.

- Key coal-based industries remain central to China’s economy, including coal-to-chemicals, and coal-based hydrogen among others. Framed as green transition strategies, they often amount to rebranded continuity rather than true transformation.

- EU policy and analysis should account for China’s underlying coal intensity, avoid equating renewable growth with full decarbonization, and strengthen cooperation on localized coal phase-out strategies.

Introduction

Optimistic headlines about China’s falling CO₂ emissions and efforts to reduce coal-fired power generation often suggest a rapid and clear path toward decarbonization, but they can obscure the structural realities of the country’s energy system and its long-term trajectory. Behind narratives highlighting record growth in renewable capacity, a different coal story remains to be told. Although China’s renewable buildout is substantial, it coexists with a large, hard-to-abate coal sector that remains deeply embedded in industrial production and the overall energy mix, underscoring the continued expansion and central role of coal in electricity generation.

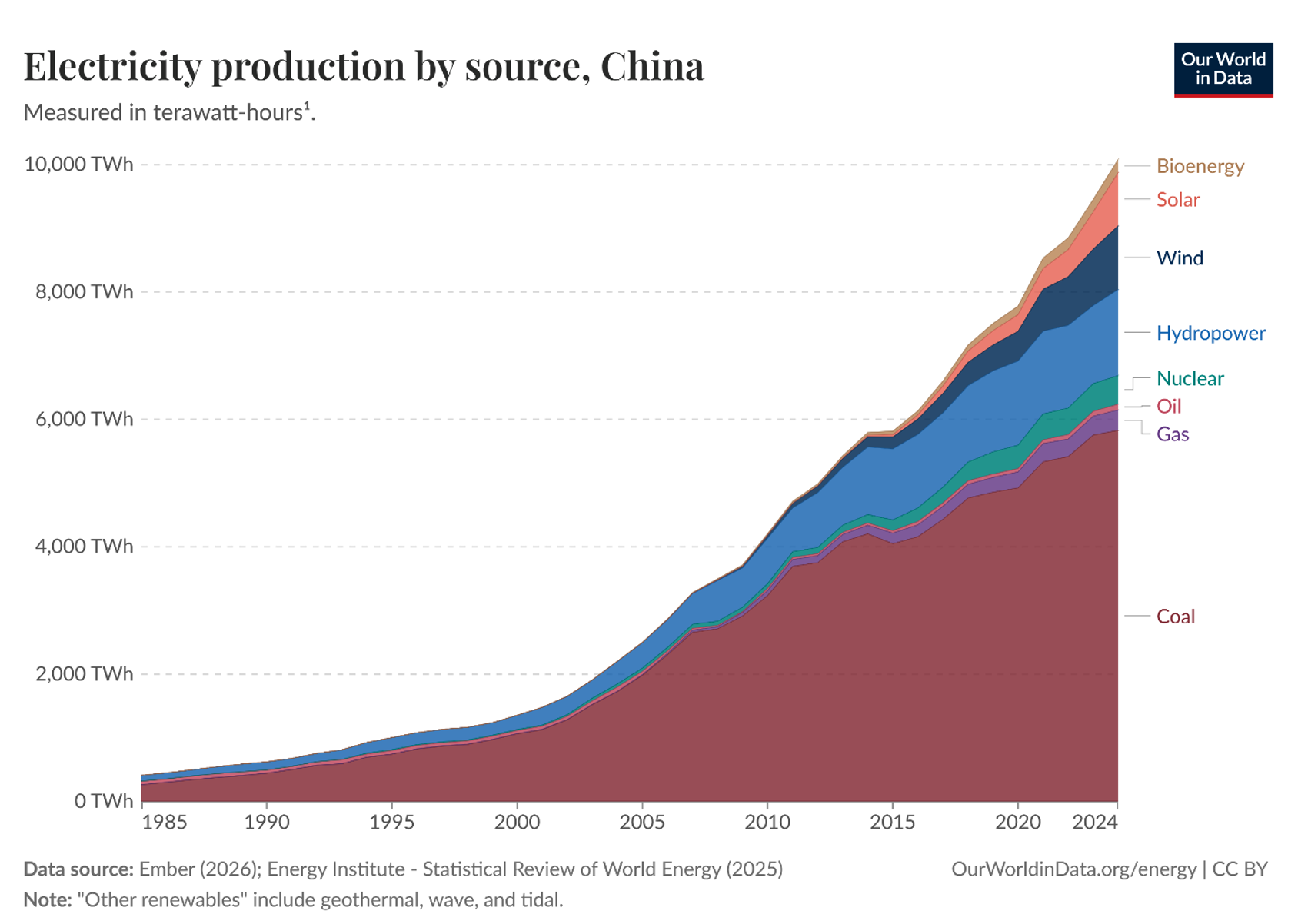

In recent years, China’s rapid expansion of renewable energy capacity has had profound effects on its traditionally coal-dominated energy system. In 2024 and 2025 alone, China installed 360 and 430 gigawatts of wind and solar capacity, respectively.[1] In 2024, this represented roughly 64% of all new solar and wind installations worldwide.[2] Most notably, as of February 2025, for the first time, wind and solar energy together – reaching a total installed capacity of 1.45 billion kW – have overtaken coal power, becoming China’s largest electricity source in terms of installed capacity.[3]

This, however, does not mean that renewable energy has already displaced thermal power[4] such as coal, despite increases in installed capacity. Chinese data, and increasingly global data, tend to report installed capacity, which indicates the potential maximum output, rather than operational or actually producing capacity. In practice, especially in China, only a fraction of installed renewable capacity is actively generating electricity at any given time due to storage limitations and grid dispatch constraints, among other factors. Consequently, when examining China’s energy mix, which reflects the energy actually consumed by society, coal energy still accounts for the majority, representing 55.5 percent of the total between October 2024 and September 2025.[5] Moreover, as China’s total energy demand continues to rise, the absolute amount of coal-fired electricity generation increased for many years and only declined for the first time in 2025, by 1.6% year on year.[6]

Fig. 1: China’s electricity production by source 1985-2024[7]

Against the backdrop of global climate targets and China’s commitments to peak carbon emissions by 2030 and achieve carbon neutrality by 2060, deep decarbonization has become an essential policy objective. Achieving these goals requires a comprehensive energy transition, as the energy sector constitutes a central source of CO₂ emissions. A key component of this transition is the gradual phase-out of coal. In China, however, the coal sector is deeply embedded in the country’s economic structures, regional development, and energy system, making a rapid exit particularly challenging. Against this background, this paper examines the current state of China’s coal sector and analyzes the economic, structural, and political challenges associated with a necessary phase-out of coal in China.

Where China’s Coal Industry Stands Today

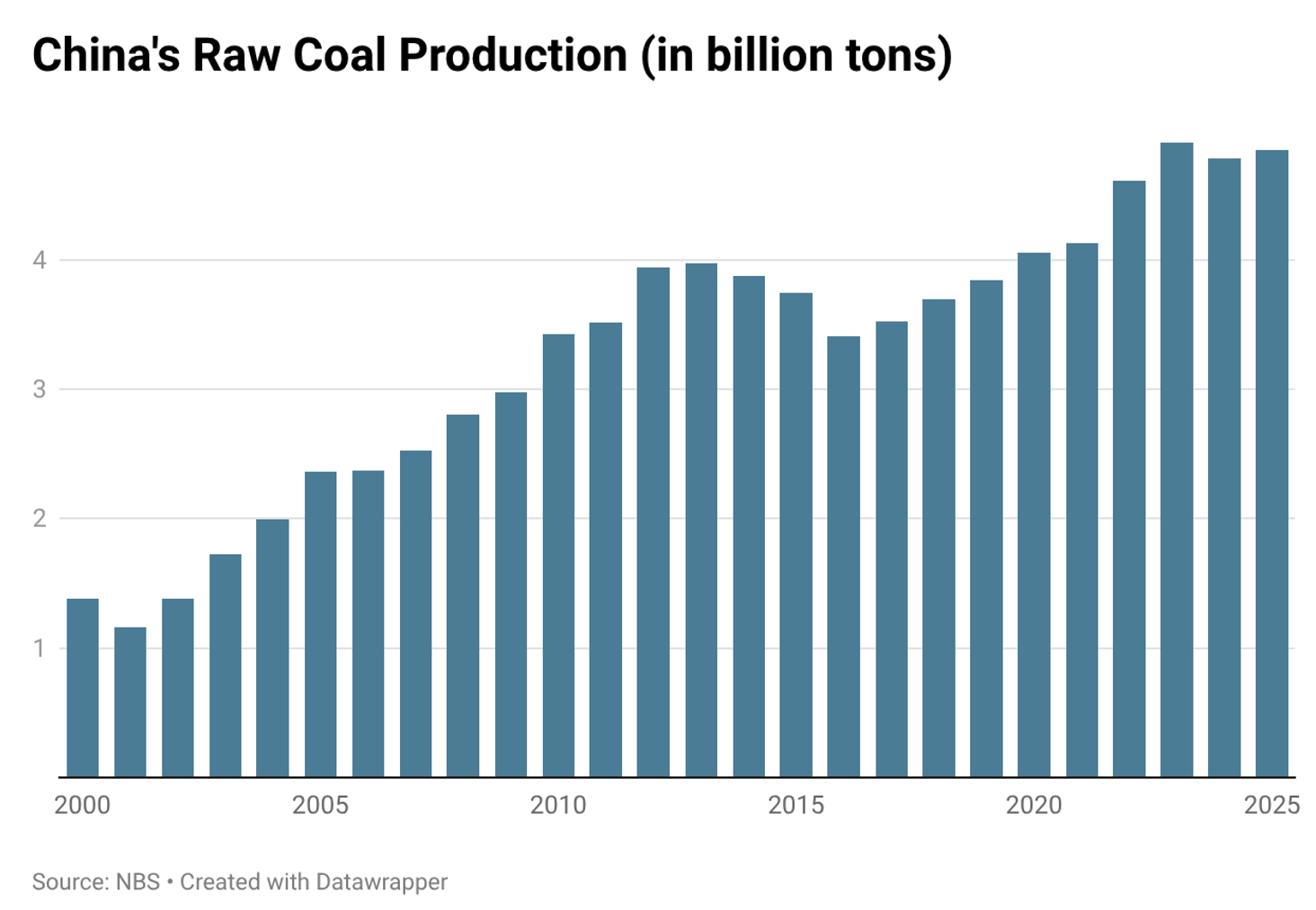

Despite China’s rapid expansion of renewable energy installations, the country has also continued building coal-fired power plants, reaching a 10-year high of 94.5 gigawatts in 2024, driven by rising energy demand and concerns over energy security.[8] In 2025, a record number of coal power plants were newly commissioned, alongside unprecedented levels of project starts and reactivations.[9] Coal mining output has likewise increased to record levels in recent years, following a period of stagnation and slight decline throughout much of the 2010s.[10] This simultaneous growth in renewables and thermal energy shows that isolated figures can be misleading without considering the full context of the country’s energy transition.

Fig. 2: China’s Raw Coal Production in billion tons 2000-2025 (Own graph based on data from the National Bureau of Statistics)

Merely in terms of coal sector employment, the situation looks clearly different. Following a series of environmental regulations and policies aimed at reducing coal overcapacity in the 2010s, numerous closures and layoffs occurred within China’s coal sector. As a result, coal employment has fallen to historically low levels in recent years, declining by around 50% between 2013 and 2022 in coal mining, washing, and dressing.[11] However, precise figures are difficult to determine, as actual employment numbers may be somewhat higher than officially recorded.

Despite declining coal employment, coal remains central to China’s energy system. The overwhelming majority of coal production is directed toward industry, where it is consumed either in its original form or as heat or electricity.[12] Consequently, China’s industry would be most affected by a structural phase-out of coal, while other end-use sectors such as residential, commercial, agricultural, and transport account for only a marginal share and would be comparatively less affected.

Thus, despite growing narratives of a ‘greening’ China driven by the rapid expansion of renewable energy, a more accurate picture recognizes the continued existence and dominance of a large, hard-to-abate coal sector. This sector continues to fuel China’s industry and remains a central component of the energy mix, even amid rising renewable capacity installations.

Tentative attempts at transformation

Despite China’s dual carbon goals – peaking CO₂ emissions by 2030 and achieving carbon neutrality by 2060 – there is still no consistent, nationwide phase-out of coal. Instead, China has implemented a series of mostly isolated decarbonization policies and emission reduction targets that are partly intended to support the dual carbon goal, but vary in strictness across regions and political priorities. Decarbonization policies include such on the closure of coal mines and coal-fired power plants, particularly smaller facilities with poor environmental standards, as well as plant and mine shutdowns aimed at reducing air pollution among others.[13] They also encompassed the closure of coal-based production capacities in the steel or aluminium sectors, or banning coal as a heating source in rural areas of northern China.[14]

The growing fiscal burden of coal-depleted cities

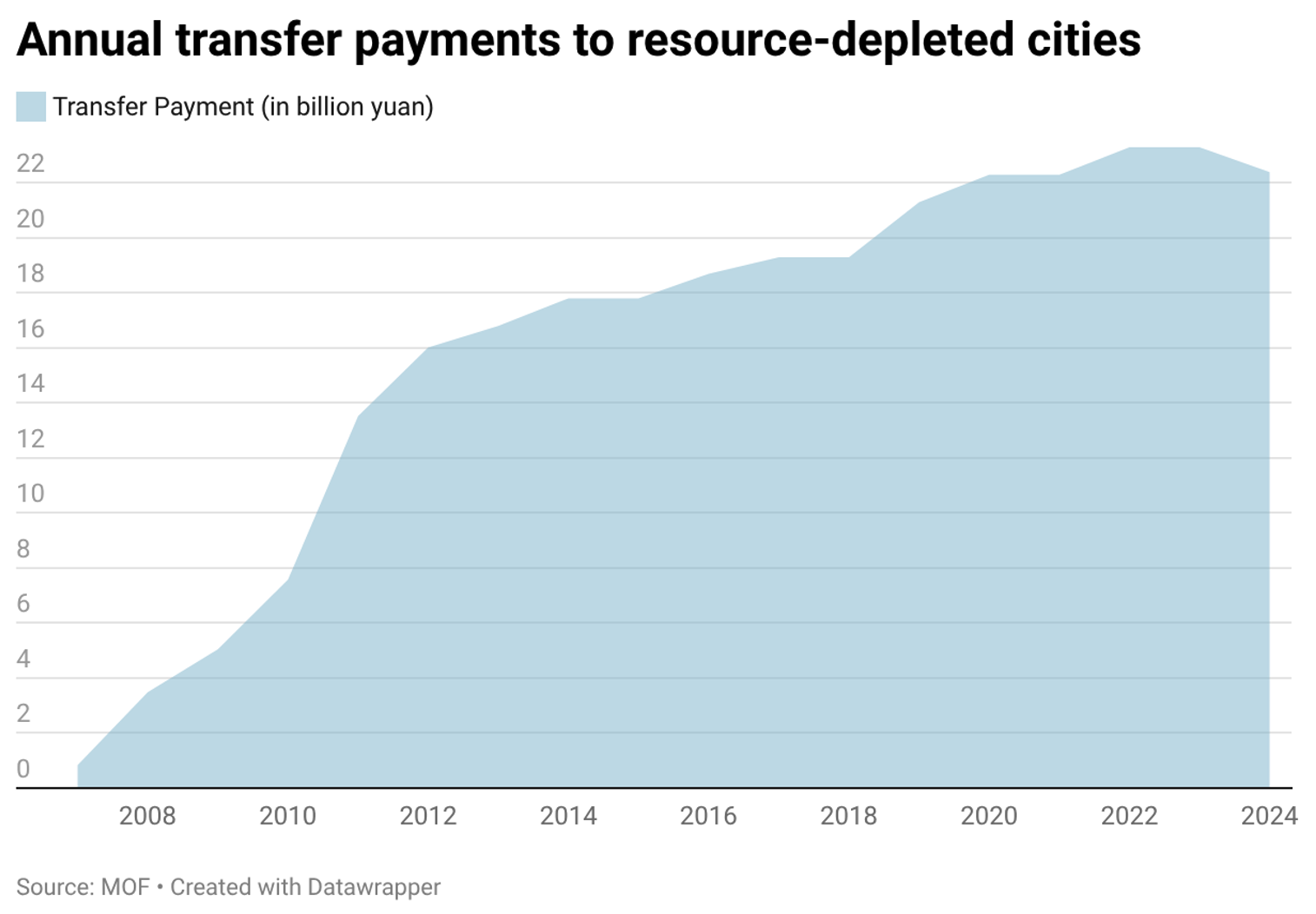

One of the most notable examples of a cross-sectoral and multidimensional policy aimed at transitioning away from coal in China so far is the transformation of coal resource-depleted cities. In the 2000s, the Chinese government began addressing the growing number of resource-depleted cities across the country, which were struggling with structural economic problems. Between 2008 and 2012, the central government officially designated 69 resource-depleted cities, including 37 coal resource-depleted cities, although the current actual number is likely much higher.[15] These officially recognized resource-depleted cities received and still receive support from the government, particularly in the form of transfer payments to support social security, education and healthcare, environmental protection, public infrastructure construction, and interest subsidies for special loans in these cities.[16] The transfer payments were conceived as time-limited from the outset, initially for three to four years from 2007 to 2010. Later, the possibility of extensions was announced, followed by plans for a phased withdrawal. In practice, however, new extension options continued to be introduced, and transfer payments to resource-depleted cities are still being made to this day.

Fig. 3: Annual transfer payments by the central government in billion RMB (Own graph based on data from the Chinese Ministry of Finance)

Although transfer payments have increased in absolute terms in recent years, when compared to the budgets of the affected cities, these payments provide limited support, and may thus not be sufficient as a long-term strategy for facilitating the transformation.[17] In this context, some cities have been reportedly unenthusiastic about applying for these transfer payments because the amounts are relatively small.[18]

Beyond financial support, these resource-depleted cities, and particularly their local governments, are expected to attract new investments or establish new industries to accelerate the economic diversification of cities that, for decades, have been overwhelmingly dependent on coal and largely monoindustrial.

Between heavy industry diversification and tourism expansion

Investment attraction remains challenging in many regions of China, partly due to the country’s overall economic slowdown and partly because local conditions, such as geographic location, infrastructure, and other factors, often limit their appeal to investors. In practice, it is primarily politically prioritized “guideline industries” that are established in these areas, as they are promoted under national industrial policies regardless of local suitability. However, these industries are frequently expanded without thorough assessments of actual demand, often resulting in overcapacity, as observed in sectors such as solar and renewable energy manufacturing or electric vehicle production.[19] In provinces like Shanxi, typical investment initiatives in cities repeatedly focus on similar sectors, including tourism, renewable energy expansion, and battery production. This pattern reflects a top-down approach to investment planning, in which comparable strategies are applied across multiple cities rather uniformly. Drawing on existing infrastructure and resources from their coal era, many resource-depleted cities have also developed more diversified heavy industries, such as the chemical industry, new materials, aluminium production, and metal smelting, among others.[20]

As a result, primarily due to the lack of alternative industries, there is often no clear or sustained shift away from coal. Development trajectories frequently revert to coal, particularly for economic reasons. This pattern is especially pronounced in cities located in traditionally coal-dependent, resource-based, and structurally weaker regions of China, making the transformation process in many coal cities particularly challenging.[21] Furthermore, the political system, including corruption, frequent turnover of local cadres, and misaligned incentives, produces varying effects on the long-term transformation process depending on the locality and specific circumstances. In some cities, local officials act as proponents of coal phase-out, while in others they function as opponents, reflecting their highly variable and context-dependent role in the transformation process.[22] Cadres often do not continue the strategies of their predecessors, which prevents long-term transformation plans from being fully implemented.[23]

The struggles of China’s indirectly coal-dependent cities

Yet, transformation efforts have not been limited to coal resource-depleted cities. Cases of coal restrictions in non-coal mining cities have revealed similar challenges, indicating that many non-coal cities, particularly heavily industrialized ones reliant on coal energy, are also likely to face a difficult transition. This is partly due to the fact that certain industrial sectors in China, such as cement, chemicals, aluminum, textiles, and others, have become structurally oriented toward coal – not necessarily because coal is essential to their production, but because state policies and cost advantages over decades have made these industries unnecessarily coal-dependent.[24]

In terms of coal consumption, for example, Shandong Province, located on China’s east coast and possessing very limited coal-mining resources, has for years recorded the second-highest level of coal consumption nationwide, after Inner Mongolia. After all, Shandong has long had high electricity demand from its dense population and economy, and especially from its large industrial base in energy-intensive sectors such as steel, cement, chemicals, and petrochemicals, supported by extensive coal-fired power generation and energy security policies that favor coal.

Consequently, even smaller cities without coal resources can experience transformation shocks comparable to those of post-mining cities when confronted with non-coal policies that mandate the closure of coal-based industrial production capacities. In Zouping, a – at least by Chinese standards – small non-mining city of 700,000 inhabitants in the Eastern province of Shandong, these policies caused its GDP to halve from one year to the next, despite the city not being a coal city in the conventional sense.[25]

Challenges in transitioning away from coal

China’s slow energy transition is largely rooted in decades of deep structural dependence on coal. Over time, coal became not just the dominant fuel but the organizing principle of China’s economy, energy system, and governance structures. This has made a shift to alternatives politically, technically, economically, and socio-economically difficult. As Chinese energy experts note, coal abundance was long treated as a self-evident justification for a coal-heavy energy mix despite international examples showing that resource abundance does not preclude diversification.[26]

This prolonged coal focus has shaped infrastructure, planning, management, and operational mechanisms, creating strong path dependence that hinders structural change and renewable deployment. It has also produced a form of “coal preference,” reinforced by symbolic and emotional reasoning and the persistent belief that coal is the cheapest option even where cost data suggest otherwise. [27] These biases are embedded in market and policy structures where coal is often favored in operations and investment, e.g. large coal units dominate baseload supply, and inefficient long-distance coal transport persists while gas and other energy alternatives are undervalued. Weak policy enforcement and entrenched interest groups further contribute to coal overcapacity, while electricity prices based on coal make it harder for alternatives to compete.[28]

Another factor underlying China’s continued reliance on coal is its broader push for greater self-reliance. In line with central government guidance to develop strategic sectors and reduce dependence on Western powers, some coal-based industries continue to receive state support rather than being meaningfully constrained by decarbonization policies. [29] Prominent examples include coal coking and coal-to-chemicals. Currently, it works in China’s favor: the steady expansion of the coal chemical sector has enabled the substitution of coal for oil, a strategy now paying off amid surging oil and gas prices driven by supply shortages. In this context, coal has effectively been assigned a geopolitical role by the state – one it is unlikely to relinquish anytime soon. It thus serves not only as an energy source but also as a tool for enhancing national self-sufficiency and reducing import dependence.[30]

Beyond the extreme dependence on coal, which already makes the energy transition particularly difficult, issues of injustice and greenwashing pose additional serious challenges. At the international level, in particular at the UN’s recent COP30, China has positioned itself as a proponent of the “just transition” concept, emphasizing that the transition should not disadvantage specific regions or actors particularly affected.[31] Domestically, China has not articulated a clear position on just transition, and the term itself is largely absent from public discourse. Nevertheless, the challenges of a just transition are very much present. In the event of a coal phase-out, China faces an exceptionally large number of coal-dependent cities and regions that would require support within the framework of an energy transition. Compared to other countries, this significantly increases the social and economic burden of transition.

The social burden of the coal transition

From a social and socio-economic justice perspective, coal sector workers are among those most affected by a coal phase-out – especially in structurally and economically underdeveloped coal provinces, where alternative employment opportunities are extremely limited. Mobility is further constrained by China’s household registration system, the hukou, which, although relaxed in recent years, still poses a barrier to migration across regions.[32]

In theory, many coal cities have announced support measures for laid-off coal workers, including retraining programs to facilitate reemployment, subsidies for enterprises that avoid or limit layoffs, support policies for unemployed workers seeking to start their own businesses, and the creation of public-interest jobs for those struggling to find new employment. In practice, however, implementation is highly uneven. Only a small number of enterprises, mostly state-owned ones, offer meaningful retraining or job placement support. Employees in privately owned mining companies are often laid off without severance pay, as they usually do not have formal long-term contracts.[33]

Regional inequality of opportunity

At the city level, injustice also manifests in uneven and often stringent support conditions from central and provincial governments. While coal resource-depleted cities may receive targeted assistance, such as transfer payments, they simultaneously face growing domestic competitive pressures, as cities with poor economic performance risk being neglected. This is illustrated by the case of Shizuishan, a coal resource-depleted city that was removed from the national-level economic development zone list in 2021 after ranking near the bottom for two consecutive years, thereby reducing its prospects for economic development. [34] In Shanxi, several cities have raised concerns about unequal support, attributing this to weak coordination at the provincial level, where resources and investment are often concentrated in the capital, Taiyuan.[35]

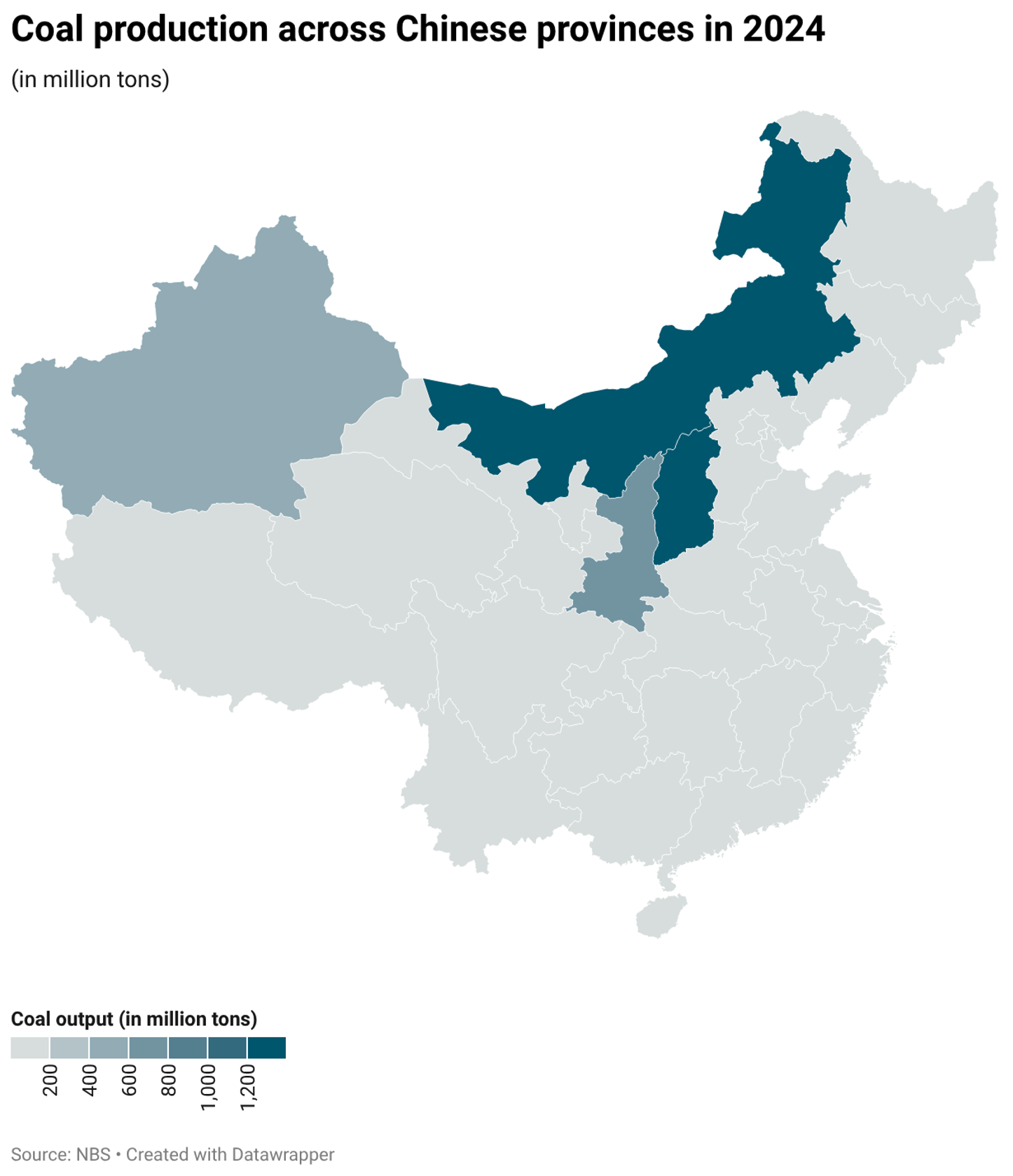

At the regional level, the coal transition is likewise marked by persistent injustices. Generally, support and resources tend to be concentrated in the politically and economically important east coast region of China, while significantly less assistance is directed to peripheral areas.[36] Historically, several provinces have long been exploited as resource hinterlands, with coal serving as the backbone of China’s rapid industrialization, while much of the generated value was not reinvested locally.[37] This dynamic is particularly evident in the resource-rich but economically and structurally underdeveloped northern provinces of Inner Mongolia, Shaanxi, and Shanxi, commonly referred to as the “coal triangle” and marked in dark blue in the map below.

Fig. 4: Coal output by province in 2024 (Own graph based on statistical data from the National Bureau of Statistics)

In Shanxi, among other coal producing provinces, decades of coal extraction were not leveraged to develop sufficient downstream industries, resulting in limited long-term economic benefits and unevenly distributed, short-term gains. Wealth accumulation was largely concentrated among a small elite of coal enterprise owners in both state-owned and private sectors, while many miners faced poor working conditions, low wages, and few alternatives as resources became depleted. Structural weaknesses, inadequate infrastructure, and the long-standing strategic neglect of western or northeastern China have further constrained these regions’ ability to attract investment, a reality often summarized by the saying that “investment does not go beyond Shanhaiguan”, meaning it won’t reach more peripheral regions of China.[38]

Green framings of coal

Beyond questions of justice, the greenwashing of the coal sector presents another major challenge to the transition. Rather than being phased out, many coal-related activities are increasingly reframed. By emphasizing technological upgrades or “green” modifications, attention is diverted from their continued dependence on coal. In Shanxi among other regions, the upgrading of the mining sector, often under the term “green mining” (绿色开采) is actively marketed as part of the transformation of coal cities, creating the impression of progress while the underlying dependence on coal remains unchanged.[39] Similar dynamics can be observed in the promotion of allegedly “green” innovations, such as hydrogen projects. In practice, much of this hydrogen is produced using coal-based processes, resulting in blue or grey hydrogen[40] rather than genuinely green alternatives. In Shanxi in particular, local and provincial governments have been actively supporting newly emerging industries and companies that produce “new energy,” for example, using by-products of coal and other fossil fuels. These initiatives are often labeled as green energy, even though they are still closely linked to the coal industry and do not fully meet the conventional definition of truly green energy.[41]

As a result, coal use continues in industrial form, but under rebranded and sanitized labels that obscure its environmental impact and undermine the actual status and development of transformation away from coal.

Conclusion

Despite China’s massive expansion of renewable energy capacity, coal remains deeply entrenched due to decades of structural dependence, the dominance of powerful state-owned enterprises, and strong vested interests at the local level. Efforts to phase out coal – particularly in resource-depleted cities – face significant obstacles, including weak alternative industries, limited private investment, and fiscal pressures that often drive local governments back toward coal-based development. Policy implementation is further undermined by fragmented governance, blurred administrative responsibilities, and incentive structures that reward officials for short-term economic performance over long-term decarbonization. As a result, coal continues to dominate many regions, increasingly concealed behind ostensibly “green” initiatives such as coal upgrading, coal-to-hydrogen projects, or efficiency improvements that do not fundamentally reduce coal dependence. This growing “greening” and rebranding of coal risks obscuring the true scale of China’s reliance on fossil fuels and underscores the need for systemic energy and governance reforms to overcome this self-reinforcing dependency.

For the European Union, this has important implications.

The EU should treat increasingly frequent optimistic headlines claiming that China has reduced CO₂ emissions or curtailed coal-fired power generation with caution, as such reports reveal little about China’s long-term decarbonization trajectory and risk misrepresenting its current energy profile. Similarly, narratives emphasizing China’s rapid expansion of renewable capacity can create an overly green impression, often leaving the continued growth of the coal sector and persistent high coal power use in the shadows.

Furthermore, many industrial products in China are still produced using coal-intensive processes, even low-carbon technology imports cannot automatically be considered “green.” The EU should therefore exercise greater caution in its trade and climate policies, recognizing the hidden coal dependence embedded in Chinese production and avoiding the assumption that rising renewable capacity necessarily translates into low-carbon output.

Finally, the EU should leverage the potential for EU–China cooperation and mutual learning on coal phase-out at the city or regional level. Partnerships between cities or provinces could be leveraged or newly established to facilitate joint projects, knowledge exchange, and practical collaboration on transitioning away from coal. Such localized initiatives could complement broader policy efforts and provide tangible models for low-carbon development, helping both sides translate ambitious climate goals into actionable outcomes.

| Funded by the European Union. Views and opinions expressed are however those of the author(s) only and do not necessarily reflect those of the European Union or European Research Executive Agency (REA). Neither the European Union nor the granting authority can be held responsible for them. |

[1] Lin, Chunting. 2026. “China’s Wind, Solar Power Installed Capacity Exceeded 1,800 GW for First Time in 2025.” Accessed April 07, 2026. https://www.yicaiglobal.com/news/chinas-wind-solar-power-installed-capacity-exceeded-1800-gw-for-first-time-in-2025.

Altieri, Katye, and Dave Jones. 2025. “Renewable Additions in 2025 Are Once Again Expected to Surge, Putting Tripling Within Reach: Renewable Additions Are Booming.” Accessed April 07, 2026. https://ember-energy.org/latest-insights/renewable-additions-in-2025-are-once-again-expected-to-surge-putting-tripling-within-reach/renewable-additions-are-booming/.

[2] n.a. 2025. “Renewable Capacity Highlights.” https://www.irena.org/-/media/Files/IRENA/Agency/Publication/2025/Mar/IRENA_DAT_RE_Capacity_Highlights_2025.pdf.

[3] Yang, Anita. 2025. “INSIGHT: China New Energy Storage Capacity to Surge by 2030.” Accessed April 07, 2026. https://www.icis.com/explore/resources/news/2025/04/14/11092303/insight-china-new-energy-storage-capacity-to-surge-by-2030/.

[4] Thermal power refers to electricity generation through the combustion of fossil fuels such as coal, oil, and natural gas. In China, coal-based energy generating capacity accounts for more than 80% of total thermal energy generating capacity making it the dominant fuel within the thermal power sector, see: Yue, Caizhou. 2025. “Zhong Dian Lian: Quanguo Suoyou Shengfen Meidian Zhuangji Zhanbi Jun Yi Jiangzhi 50% Yixia (中电联:全国所有省份煤电装机占比均已降至50%以下) [CEC (China Electricity Council): The Share of Coal Power Installed Capacity Has Fallen Below 50% in All Provinces Nationwide].” Beijing bao, April 25. https://baijiahao.baidu.com/s?id=1830370321927331152&wfr=spider&for=pc.

[5] n.a. 2026. “Electricity in People's Republic of China in 2025.” Accessed April 07, 2026. https://lowcarbonpower.org/region/People%27s_Republic_of_China.

[6] Myllyvirta, Lauri. 2026. “Analysis: Coal Power Drops in China and India for First Time in 52 Years After Clean-Energy Records.” Carbon Brief, January 13. https://www.carbonbrief.org/analysis-coal-power-drops-in-china-and-india-for-first-time-in-52-years-after-clean-energy-records/.

[7] Our World in Data. 2025. “Electricity Production by Source, China.” Accessed April 08, 2026. https://ourworldindata.org/grapher/electricity-prod-source-stacked?country=~CHN.

[8]Patel, Anika. 2025. “China’s Construction of New Coal-Power Plants ‘Reached 10-Year High’ in 2024.” Accessed April 07, 2026. https://www.carbonbrief.org/chinas-construction-of-new-coal-power-plants-reached-10-year-high-in-2024/.

[9] Qin, Qi, Christine Shearer, and Belinda Schaepe. 2026. “Built to Peak: Coal Power Expansion Runs Out of Room in China.” Accessed April 07, 2026. https://energyandcleanair.org/publication/built-to-peak-coal-power-expansion-runs-out-of-room-in-china/.

[10] Senz, Anja. 2021. “China’s Environmental and Climate Change Policies.” IDEES (52). https://revistaidees.cat/en/chinas-environmental-and-climate-change-policies/. Accessed April 07, 2026.

n.a. 2018. “China Kohleproduktion.” Committee on Electronic Information and Communication CEIC), June 1. https://www.ceicdata.com/de/indicator/china/coal-production.

Han, Winnie. 2025. “NBS: China's 2024 Coal Output Hits Record High.” Mysteel Global Pte Ltd, January 17. https://www.mysteel.net/news/5074522-nbs-chinas-2024-coal-output-hits-record-high.

[11]Yang, Yingxia, Wenjuan Dong, and Jiejie Hui. 2024. “A Just Transition for Coal Regions: Learning from Two Coal Cities in Western China.” https://www.belfercenter.org/sites/default/files/2024-06/Yang%20Dong%20Hui_China%20Just%20Coal%20Transition.pdf.

[12]International Energy Agency. 2023. “Energy Sankey China.” Accessed April 08, 2026. https://www.iea.org/data-and-statistics/data-tools/energy-sahttps://www.iea.org/data-and-statistics/data-tools/energy-sankey.

[13] Yang, Yingxia, Wenjuan Dong, and Jiejie Hui. 2024. “A Just Transition for Coal Regions: Learning from Two Coal Cities in Western China.” https://www.belfercenter.org/sites/default/files/2024-06/Yang%20Dong%20Hui_China%20Just%20Coal%20Transition.pdf.

[14] Lew, Linda. 2019. “China’s Plan to Reduce Use of Coal for Heating in Northern Homes Still Facing Problems, Report Says.” South China Morning Post, November 10. https://www.scmp.com/news/china/society/article/3037119/chinas-plan-reduce-use-coal-heating-northern-homes-still-facing.

[15] Guowuyuan Guanyu Cujin Ziyuanxing Chengshi Kechixu Fazhan De Ruogan Yijian(国务院关于促进资源型城市可持续发展的若干意见) [Opinions of the State Council on Promoting Sustainable Development of Resource-Based Cities]. Guo wu yuan (国务院). 2007. https://www.gov.cn/zhengce/zhengceku/2008-03/28/content_4941.htm.

[16] Ibid.

[17] n.a. 2011. “Shei Jiang Chengwei Disan Pi Ziyuan Kujie Chengshi? (谁将成为第三批资源枯竭城市?) [Who Will Become the Third Batch of Resource-Exhausted Cities?].” Accessed April 08, 2026. http://www.chinareform.net/plus/view.php?aid=3168.

[18] Ibid.

[19] Hawkins, Amy. 2025. “China’s Coal Heartland Fighting for a Greener Future.” The Guardian, July 9. https://www.theguardian.com/world/2025/jul/09/chinas-coal-heartland-fighting-for-a-greener-future.

[20] Yang, Yingxia, Wenjuan Dong, and Jiejie Hui. 2024. “A Just Transition for Coal Regions: Learning from Two Coal Cities in Western China.” https://www.belfercenter.org/sites/default/files/2024-06/Yang%20Dong%20Hui_China%20Just%20Coal%20Transition.pdf.

[21] Ibid.

[22] Tan, Hao, Elizabeth Thurbon, Sung-Young Kim, and John A. Mathews. 2021. “Overcoming Incumbent Resistance to the Clean Energy Shift: How Local Governments Act as Change Agents in Coal Power Station Closures in China.” Energy Policy 149. https://doi.org/10.1016/j.enpol.2020.112058.

[23] n.a. 2021. “Renkou Liushi De San Si Xian Chengshi: Datong Loushi Jiang Ying Bianju? (人口流失的三四线城市:大同楼市将迎变局?)[Third- and Fourth-Tier Cities with Population Outflow: Will Datong’s Housing Market Face a Turning Point?].” Accessed April 08, 2026. https://baijiahao.baidu.com/s?id=1714212116607664310&wfr=spider&for=pc.

[24] Global Energy Monitor. 2021. “Zhongguo Lü Gongye Yu Meidian (中国铝工业与煤电) [China’s Aluminum Industry and Coal Power].” February 13. https://www.gem.wiki/%E4%B8%AD%E5%9B%BD%E9%93%9D%E5%B7%A5%E4%B8%9A%E4%B8%8E%E7%85%A4%E7%94%B5.

Zhang, Shuwei. 2024. The Power System in Transformation and That Will Change China: Ontology and Epistemology. Beijing: Jingji guanli chubanshe.

[25] Ibid.

[26] Zhang, Shuwei. 2024. The Power System in Transformation and That Will Change China: Ontology and Epistemology. Beijing: Jingji guanli chubanshe.

[27] Ibid.

[28] Ibid.

[29] Zhao, Murphy. 2026. “This Is Not China’s War, but Beijing Started Preparing for It Years Ago.” New York Times, April 7. https://cn.nytimes.com/business/20260407/china-oil-shock-iran-war/dual/.

[30] Ibid.

[31] The term “just transition” originated in the 1970s within the U.S. labor movement, initially referring to protecting workers during economic and energy shifts. Since the 2000s, its meaning has broadened to include environmental, climate, and energy justice, with a focus on fairly distributing costs and benefits and ensuring equitable participation in decision-making, see: Yang, Yingxia, Wenjuan Dong, and Jiejie Hui. 2024. “A Just Transition for Coal Regions: Learning from Two Coal Cities in Western China.” https://www.belfercenter.org/sites/default/files/2024-06/Yang%20Dong%20Hui_China%20Just%20Coal%20Transition.pdf.

[32] Over the past few decades, China’s hukou system has gradually become more flexible, with relaxations in the urban-rural divide, promotion of points-based systems that allow citizens to obtain an urban hukou if they meet certain criteria such as education, occupation, tax payments and age, etc. See CECC. 2012. “Recent Chinese Hukou Reforms.” Accessed April 08, 2026. https://www.cecc.gov/recent-chinese-hukou-reforms.

[33] Yang, Yingxia, Wenjuan Dong, and Jiejie Hui. 2024. “A Just Transition for Coal Regions: Learning from Two Coal Cities in Western China.” https://www.belfercenter.org/sites/default/files/2024-06/Yang%20Dong%20Hui_China%20Just%20Coal%20Transition.pdf.

[34] Hao, Dafeng. 2021. “Lianxu Liang Nian Paiming Daosu, Ningxia Shizuishan Bei "Kaichu" Chu Guojia Ji Jingkaiqu Xilie (连续两年排名倒数,宁夏石嘴山被“开除”出国家级经开区序列) [After Ranking at the Bottom for Two Consecutive Years, Shizuishan in Ningxia Has Been “Expelled” from the National-Level Economic Development Zone Lineup].” Fenghuang Wang, January 27. https://finance.ifeng.com/c/83NJY9QKynK.

[35] n.a. 2021. “Shanxi Shuozhou Shi Yi Zuo Hao Wu Xiwang De Chengshi Ma? (山西朔州是一座毫无希望的城市吗?) [Is Shuozhou in Shanxi a City Without Any Hope?].” Accessed April 08, 2026. https://www.163.com/dy/article/GF7OL8KP0534QGRW.html.

[36] n.a. 2021. “Ruhe Dazao Yi Ge "Qiang Shenghui" Taiyuan? (如何打造一个“强省会”太原?) [How to Build a “Strong Provincial Capital” in Taiyuan?].”Meiri jingji xinwen, November 1. https://baijiahao.baidu.com/s?id=1715241717151851800&wfr=spider&for=pc.

n.a. 2022. “Thinking That “Investments Do Not Go Beyond the Shanhaiguan Pass” Causes Immeasurable Harm to the Northeast.” Accessed April 08, 2026. https://mjyu.lnu.edu.cn/info/1045/2193.htm.

[37] Guowuyuan Guanyu Yinfa Quanguo Zhuti Gongnengqu Guihua De Tongzhi (国务院关于印发全国主体功能区规划的通知) [Notice of the State Council on Issuing the National Main Functional Area Planning]. Guowuyuan. June 9, 2011. Accessed April 08, 2026. https://www.mee.gov.cn/zcwj/gwywj/201811/t20181129_676510.shtml.

[38] n.a. 2022. “Thinking That “Investments Do Not Go Beyond the Shanhaiguan Pass” Causes Immeasurable Harm to the Northeast.” Accessed April 08, 2026. https://mjyu.lnu.edu.cn/info/1045/2193.htm.

[39] State-owned Assets Supervision and Administration Commission of Shanxi Provincial Government. 2017. “Shanxi Jiaomei: Zhu Lu Er Xing Zhuanxing Shengji (山西焦煤:逐绿而行转型升级) [Shanxi Coking Coal: Moving Toward Green Development and Industrial Transformation].” Accessed April 08, 2026. https://gzw.shanxi.gov.cn/xwfb/qyfz/202406/t20240613_9587717.shtml.

[40] Hydrogen can be produced through a variety of methods, commonly referred to as different “colours.” Among these, green hydrogen is the only type that is produced in a climate neutral way, whereas blue and grey hydrogen are fossil-based. (De Blasio, Nicola. 2024. “The Colors of Hydrogen.” Belfer Center, July 8. https://www.belfercenter.org/research-analysis/colors-hydrogen.)

[41] n.a. n.d. “Shengtai Huanjing Bu Yaoqing Minying Qiye Daibiao Zuotan! Zhudong Xiangying Lvse Fazhan Haozhao, Shanxi Pengfei Jituan Jiesheng Touzi Jin 2 Yi Yuan… (生态环境部邀请民营企业代表座谈!主动响应绿色发展号召,山西鹏飞集团节省投资近2亿元……) [The Ministry of Ecology and Environment Invited Representatives of Private Enterprises for a Discussion! Actively Responding to the Call for Green Development, Shanxi Pengfei Group Saved Nearly 200 Million Yuan in Investment…].” Accessed April 08, 2026. https://news.sohu.com/a/1000183381_395101.